Is HMRC at breaking point?

After it feels like we've spent more time in the telephone queues of HMRC than anything else - we ask why HMRC service levels are slipping

TAX TIPS

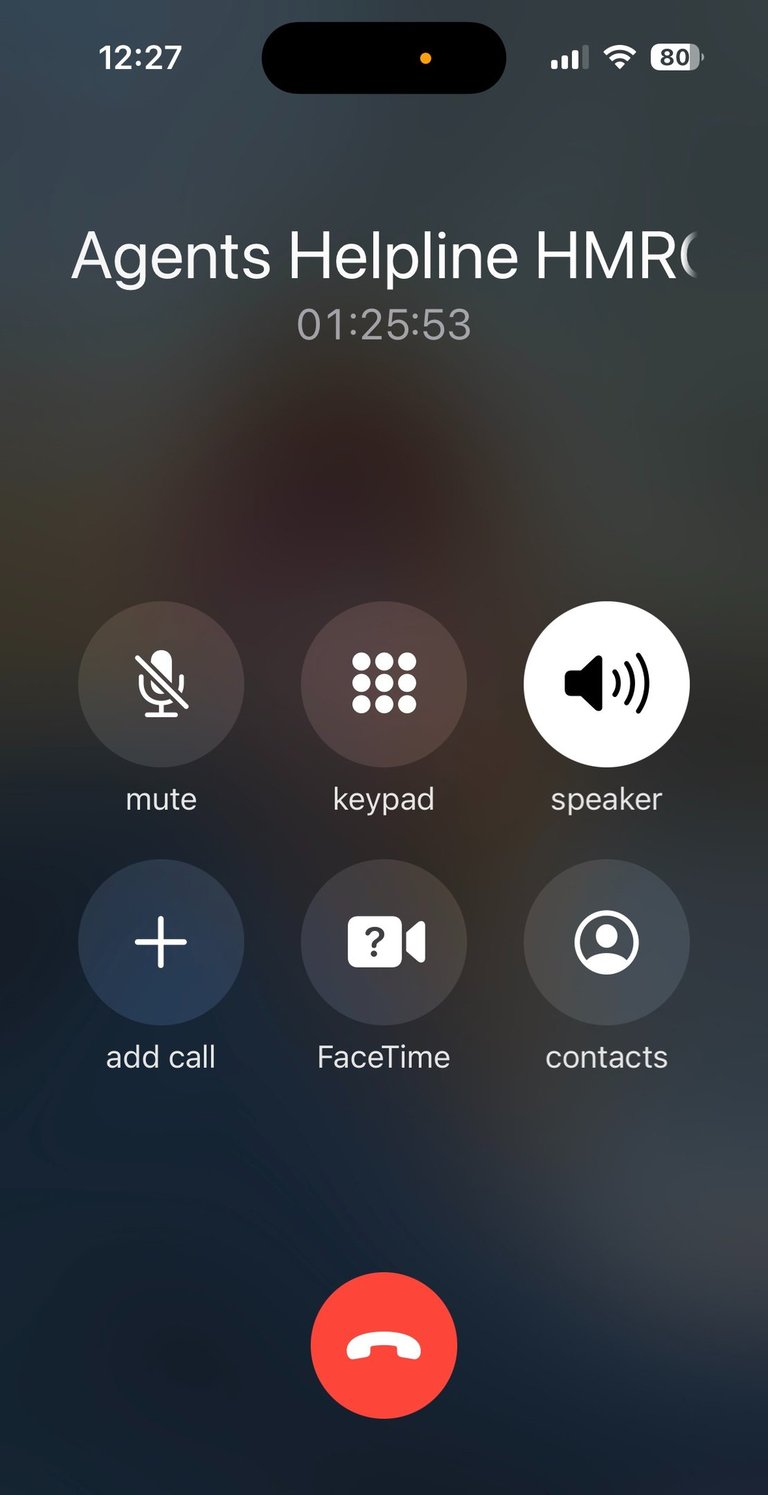

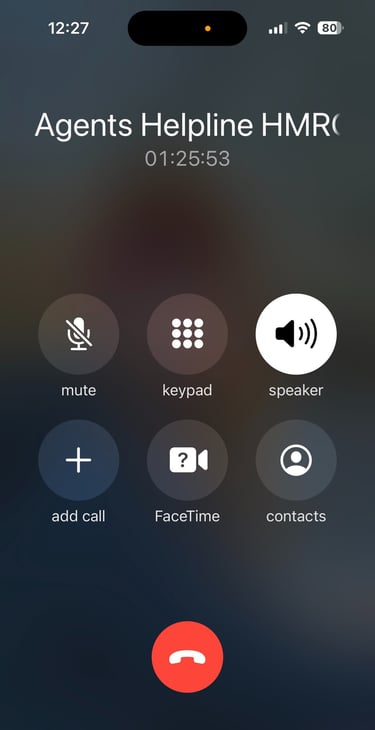

One hour and twenty five minutes. A short amount of time if you're talking about the running time of a movie and less than the time it takes for a Premier League football match to be played. But what about if the one hour and twenty five minutes is the length of time it takes to get through to HMRC on their "Agent Dedicated Line"?

Today we had reason to call HMRC in order to chase progress on correspondence that we had sent for a number of clients (more on that later...) and that was the time it took for us to reach HMRC so that we could speak to an advisor.

Aside from the awful hold music (isn't all hold music awful?) the distraction that you have while waiting for a call to answered can't help but reduce your productivity during this time. We've all been there - you can't quite switch off from the call as once you're that deep into a queue, you don't dare look away for a moment in case the call is answered.

Our team have had a torrid time trying to speak with HMRC on behalf of a number of our clients this week. When we were able to speak with an advisor it was shocking to hear the current service levels HMRC expect to provide.

Once through and able to speak to the advisor, she was apologetic and said that the lines were busier than usual. We were then told the same thing that the automated message told us at the start of our call: that we would not be able to discuss progress chasing as HMRC were experiencing a higher volume of calls than usual.

Given that for one client we were looking for an update on correspondence that was originally sent to HMRC in September 2022 (and chased via further correspondence a number of times since) in respect of a letter from HMRC themselves stating that our client should have filed a CGT Return on the sale of a UK residential property, we decided to push on regardless to see if we could get some answers.

The timescale given in response to our questions of when we should expect a full reply or even an acknowledgement to set our client's mind at ease was more shocking than the 85 minutes worth of hold music.

Here is what we were told:

Neither our original nor our chasing letters from 2022 had been actioned, nor had they been allocated for action as yet.

The timescale to have this allocated and actioned was hoped to be 20 weeks from receipt of the post.

We needed to wait 2 more weeks before the advisor could do anything as the latest noted correspondence was received only 18 weeks ago.

And here we were thinking that our telephone call had taken some time to answer.

On to the next...

For the next client, we had sent a paper Capital Gains Tax Return to HMRC due to the fact that our client did not have the required information / documents to register for an online CGT Account with HMRC. Once again, we were looking for an update on correspondence that was originally sent to HMRC in 2022.

The timescale given was the same as that of the previous client, being a hoped 20 week turnaround. However, this time we had passed this projected response time. So, what now?

Here is what we were told:

As this was a tax return, this should be prioritised.

As such, the advisor would be allocating this item of post to a "special team" so that it can be processed.

The timescale to have this actioned was now 10 working days.

We now needed to wait for 10 working days to elapse, then if we haven't had a response to call again to see what is happening.

We were further told that for this issue HMRC would not contact us or the client in any other way than providing a written response to the correspondence.

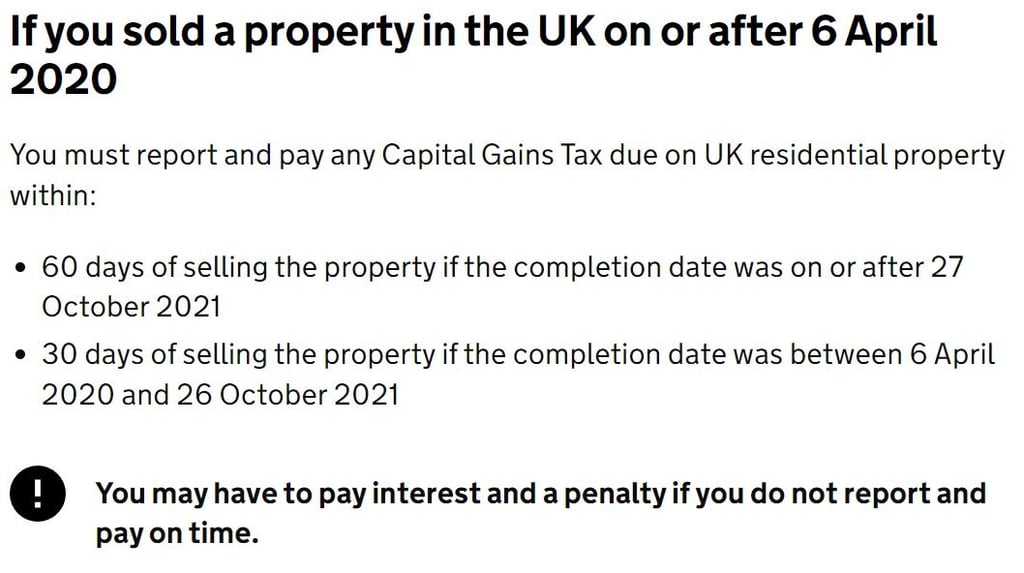

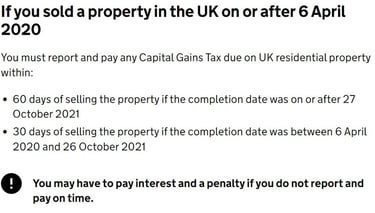

What concerns us about these timescales when it comes to reporting any CGT on the sale of UK residential property (both clients mentioned above had sold such properties) is the deadlines to which HMRC expect actions to be taken by our clients, as shown below:

"If you sold a property in the UK on or after 6 April 2020

You must report and pay any Capital Gains Tax due on UK residential property within:

60 days of selling the property if the completion date was on or after 27 October 2021

30 days of selling the property if the completion date was between 6 April 2020 and 26 October 2021"

So, HMRC demand that someone who is required to report (and pay!) their CGT due on the sale of a UK property within 60 days (down from the previous 30 days). Yet HMRC hope to be able to provide a response to any paper CGT Returns or CGT correspondence by 140 days. An extra 80 days for HMRC to complete their work (a target which clearly is not being hit in our experience), then an additional 10 working days to be dealt with by a "special team"? So potentially 150+ days for HMRC compared to 60 for our clients.

Surely we are not the only ones who find this to be somewhat unfair on those of our clients who would face financial penalties should they not meet the 60 day deadline. While all clients will strive to meet such deadlines and with our help would certainly do so, this is still a relatively new way of reporting CGT to HMRC.

We cannot hep but feel that a further rethink is on order in terms of the reporting and payment of CGT on the sale of UK residential property.

We have been full of praise in the past (and we still are) in terms of the online CGT Filing system. This system is so much easier to use than the traditional Self-Assessment Online Returns - especially for obtaining authority to file on the behalf of a client which can be completed in a matter of minutes compared to waiting weeks at times for Self-Assessment.

So why is there such a delay in dealing with correspondence? When it comes to physical correspondence relating to CGT, we can't help but think that HMRC severely underestimated the volume of paper CGT returns and written correspondence that would be required. After investing what must have been a decent sum in developing the online system, perhaps they thought that this would capture everything from everyone who would be required to file. Not so, it seems.

Our recommendations?

Keep the CGT online filing system, it is a (relative) joy to use and when it fits to the circumstances of a client and when it works, then it works really well.

Take away the requirement to file the CGT Return within 60 days. Mirror the usual Self-Assessment online filing deadline of 31st January following the end of the tax year in which the property was sold. If a paper return is required, then have this mirror the deadline of 31st October following the end of the tax year in which the property was sold.

Take away the requirement to pay the CGT due within 60 days. Revert back to the usual Self-Assessment payment deadline of 31st January following the end of the tax year in which the property was sold.

This would ease the burden on both the taxpayer and on HMRC, so everyone wins - right?

Not quite. While the above recommendations seem to be sensible for both sides, we can't see the changes being considered seriously.

Why? Having CGT reported and paid within 60 days of the sale of a UK residential property allows the Treasury to receive the CGT due much more quickly than if the CGT had to be paid within the same timescales as Self-Assessment.

For example, if I was to sell a UK residential property today and there was a resulting CGT liability then under the current regime I have to file a CGT Return online and pay my CGT liability by 27th June 2023.

However, if we were to revert to the Self-Assessment payment deadline, then the CGT liability would not be due and payable until 31st January 2025 - some 19 months later.

Or if we wanted to be cheeky, in the additional time that it would take to pay the CGT liability, HMRC would have time to have responded to 4 CGT letters / paper returns. We would never be so facetious though.

While the reasoning for introducing the new CGT regime was twofold - reducing the Self-Assessment administrative burden of requiring someone who needed to report CGT on UK residential property and also ensuring that the Treasury receives the CGT liability earlier.

Clearly the more important driver in the current financial climate will be the earlier receipt of money into the coffers. Perhaps money that could be spent bolstering HMRC's ability to deal with post in a timely fashion? We can but hope.

Contact Us

Contact us today on freephone 0800 0016 878 for a free consultation on all tax issues, or fill out the handy form below and we'll get back to you as soon as possible.

Alternatively, you can email us at info@thetaxfaculty.co.uk or complete the form below.

(Please note, non-UK callers may need to call 0207 101 3845 if your line cannot connect to our 0800 number)

Feel free to contact us through WhatsApp - we accept calls and messages.

Simply click the WhatsApp button below:

The Tax Faculty LLP - info@thetaxfaculty.co.uk

Call us on 0800 0016 878 for a free consultation

Copyright © 2026 The Tax Faculty LLP - All Rights Reserved