Capital Gains Tax on Inherited Property - Do I have to pay?

After reviewing some online "guidance" we thought it would be good to share information on Private Residence Relief on Inherited properties

TAX TIPS

Today we had a client contact us in order to request assistance in dealing with the tax impact of selling a property that they had inherited some decades ago.

As with most conversation with clients, this gentleman had done some background reading and research into his circumstances before picking up the telephone to clarify his understanding. While we recommend doing as much research as possible, the internet can be a very dangerous place when it comes to any type of advice - more so when it comes to tax!

The main topic of conversation was whether Principle Private Residence ("PPR") relief was due on the sale of the property. PPR relief is a common theme to be considered when dealing with the Capital Gains Tax ("CGT") liability on the sale of any residential property, not just those that were inherited, so we were well prepared to deal with a number of questions and misconceptions about PPR relief.

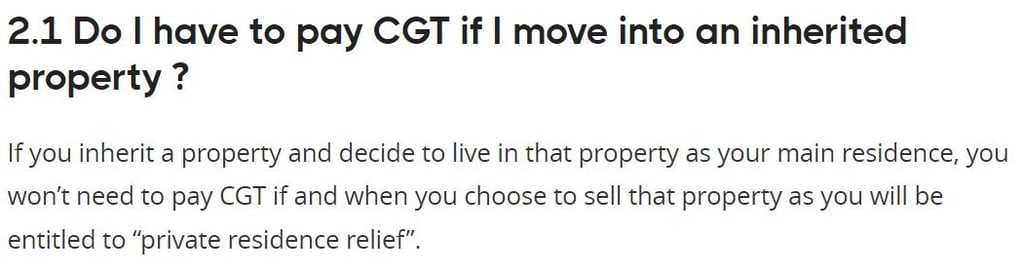

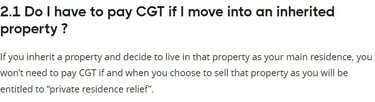

First, for a little context, the client directed us to a website which states:

Following a conversation with a client recently, we thought that it would be helpful to tackle a few of the myths surrounding Principle Private Residence Relief on the sale of an inherited property.

From this guidance the client was absolutely convinced that as he had lived in the property, he was entitled to PPR relief on the sale of the property that he had inherited and therefore would not pay any CGT.

Was this actually the case?

No, in fact this was not the case. In this instance our client had only lived in the property for a relatively short time during his period of ownership - some 3 years out of a total of 22 years of ownership.

Was PPR relief due?

Yes, but as we have discussed with many clients, PPR relief is proportional rather than being an all or nothing relief. Our client is entitled to PPR relief for the period that he resided in the property (and the final 9 month period allowed by statute) but this does not relieve him from paying CGT on the gain which resulted from his sale of the property.

There are a number of additional factors which at times allows us to extend the proportion of PPR relief due on the sale of a property and we have successfully claimed such extended periods for our clients, however this is due to the circumstances of the individual.

What concerns us about the guidance above is that this was taken from a website which appears on the first page when conducting a Google search into CGT on inherited properties, so it is no wonder that clients may be confused.

One of the reasons that we decided to specifically tackle PPR relief in relation to inherited properties is that many clients come to us thinking that they will not need to pay CGT, or will pay a lower amount of CGT, due to their having previously lived in the property as their main residence.

Again, some of the guidance out there is unclear on this aspect so it is no wonder that clients can become confused.

What is important to remember here is that when selling a property that you own personally, PPR relief is only available if you lived in the property during your period of ownership.

This impacted a recent client who had been told that PPR relief was available on the sale of their childhood home which they had inherited when her mother and father had passed away.

The client was under the impression that as she had lived in the property as a child, then at least partial PPR relief was due.

Unfortunately this was not the case as our client had not lived in the property since it was inherited - which was the beginning of her period of ownership.

While this was obviously disappointing for our client, she now had clarity over her CGT circumstances following the sale of the property in question.

If you require assistance with the CGT consequences of the sale of a property that you have inherited, please feel free to contact us on info@thetaxfaculty.co.uk or call us free on 0800 0016 878 for a free initial consultation.

Contact Us

Contact us today on freephone 0800 0016 878 for a free consultation on all tax issues, or fill out the handy form below and we'll get back to you as soon as possible.

Alternatively, you can email us at info@thetaxfaculty.co.uk or complete the form below.

(Please note, non-UK callers may need to call 0207 101 3845 if your line cannot connect to our 0800 number)

Feel free to contact us through WhatsApp - we accept calls and messages.

Simply click the WhatsApp button below:

The Tax Faculty LLP - info@thetaxfaculty.co.uk

Call us on 0800 0016 878 for a free consultation

Copyright © 2026 The Tax Faculty LLP - All Rights Reserved